ARTICLE SUMMARY:

More than a decade of struggle, followed by FDA approval of its TOPS facet joint replacement system has led Premia to the brink of success, with a coveted superiority claim for what is the first device of its kind to reach the market. That’s an important milestone, but commercial challenges loom as it launches an inpatient only procedure into a consolidating market that has seen its share of disappointments.

It’s not an uncommon trajectory even for successful innovators in spine surgery: decades of hard work and hype toward achieving an ambitious vision of an alternative to lumbar spine fusion, a common and frustratingly problematic surgical option for back pain, financial and commercial setbacks with investors circling in and out, and multiple high-risk checkpoints.

A small subset of start-ups meets its goals, with success defined by FDA PMA approval for an innovative technology, and an even smaller group reaps the benefits of a superiority claim. Then comes the inevitable question: what’s next?

That’s the turning point where Premia Spine now finds itself. Nearly 20 years after it began working on an artificial joint as an alternative to lumbar fusion surgery, the company has received FDA PMA approval with a superiority claim for its TOPS (Total Posterior Spine) facet joint replacement system—the only lumbar spine device to get such a claim on its label. The approval is for stabilizing the spine for patients with Grade 1 degenerative spondylolisthesis and spinal stenosis, based on two-year data from a randomized, controlled prospective investigational device exemption (IDE) clinical trial comparing patients who underwent a lumbar TOPS facet arthroplasty with a control group that received a standard transforaminal lumbar interbody fusion (TLIF). The device fills a gap for a huge patient population of more than 100 million worldwide in a controversial area of care that is the bread and butter of spine surgeons’ practice.

About a third of all lumbar fusion patients globally, or 350,000 people, are likely to be eligible, based on a diagnosis of lumbar spinal stenosis due to degenerative spondylolisthesis, representing a $2 billion opportunity, estimates Premia’s CEO and founder Ron Sacher, who along the way has carefully navigated through multiple high-risk, key decision points that he hopes position the company well in an area of medicine prone to disappointment and hype.

“The TOPS facet arthroplasty has a place in the treatment of degenerative Grade 1 spondylolisthesis, primarily because it creates an opportunity to treat patients with this disorder without a fusion but with some stabilization of the spondylolisthesis,” says Zoher Ghogawala, MD, PhD, chair of neurosurgery at Lahey Hospital and Medical Center in Burlington, MA, and a professor of neurosurgery at Tufts University School of Medicine.

“Its biggest advantage is that it has the potential to provide stability without fusion in this condition, which may reduce the risk of reoperations in the future for patients who have this kind of problem,” he continues, adding that, given the small data set upon which the approval is based, much more research is needed to confirm lower risk of reoperations, and also to better understand some of the trial results, notably the high incidence of fusion failures in the control group (TLIF patients).

Ghogawala’s assessment carries weight because he is a nationally recognized expert at the heart of one of the biggest controversies in spine surgery today—the debate over whether treatment with decompression alone (lumbar laminectomy) or decompression with fusion (lumbar laminectomy with instrumented pedicle screw fusion) achieves better outcomes for patients with certain kinds of lower back pain (Grade 1 spondylolisthesis with spinal stenosis patients who fail conservative [non-surgical] therapies). He served as the national principal investigator on the recently completed high-profile SLIP study—a randomized controlled trial published in the New England Journal of Medicine that compared both approaches, finding in favor of lumbar laminectomy with fusion. That said, other studies, largely in Europe, have come to the opposite conclusion. (See “The Controversy Over Decompression Vs. Fusion: What the Data Tells Us,” MedTech Strategist, December 30, 2021.) The downstream effect of fusion is that the procedure can cause higher rates of adjacent segment disease (ASD), which requires a reoperation to correct.

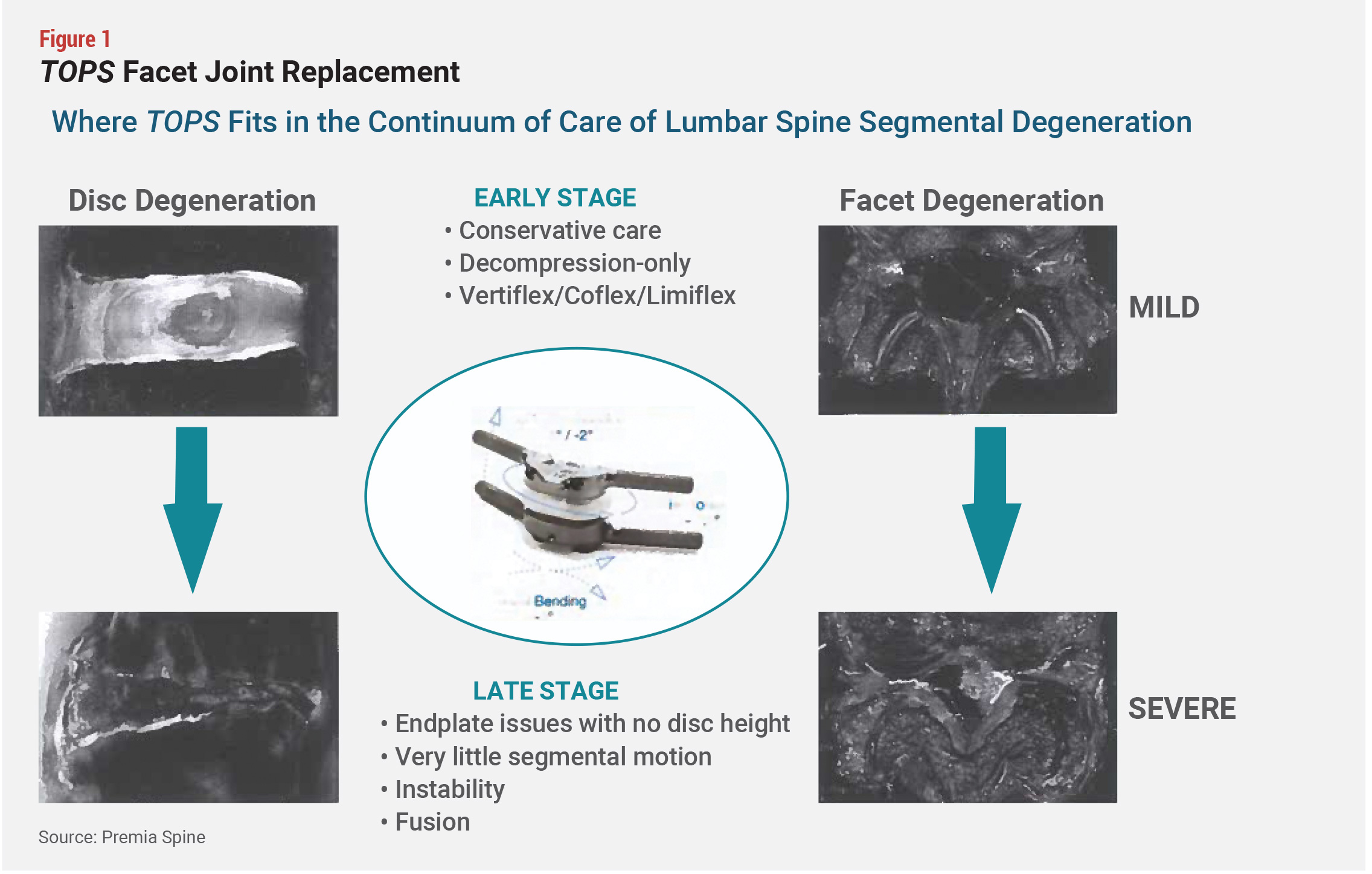

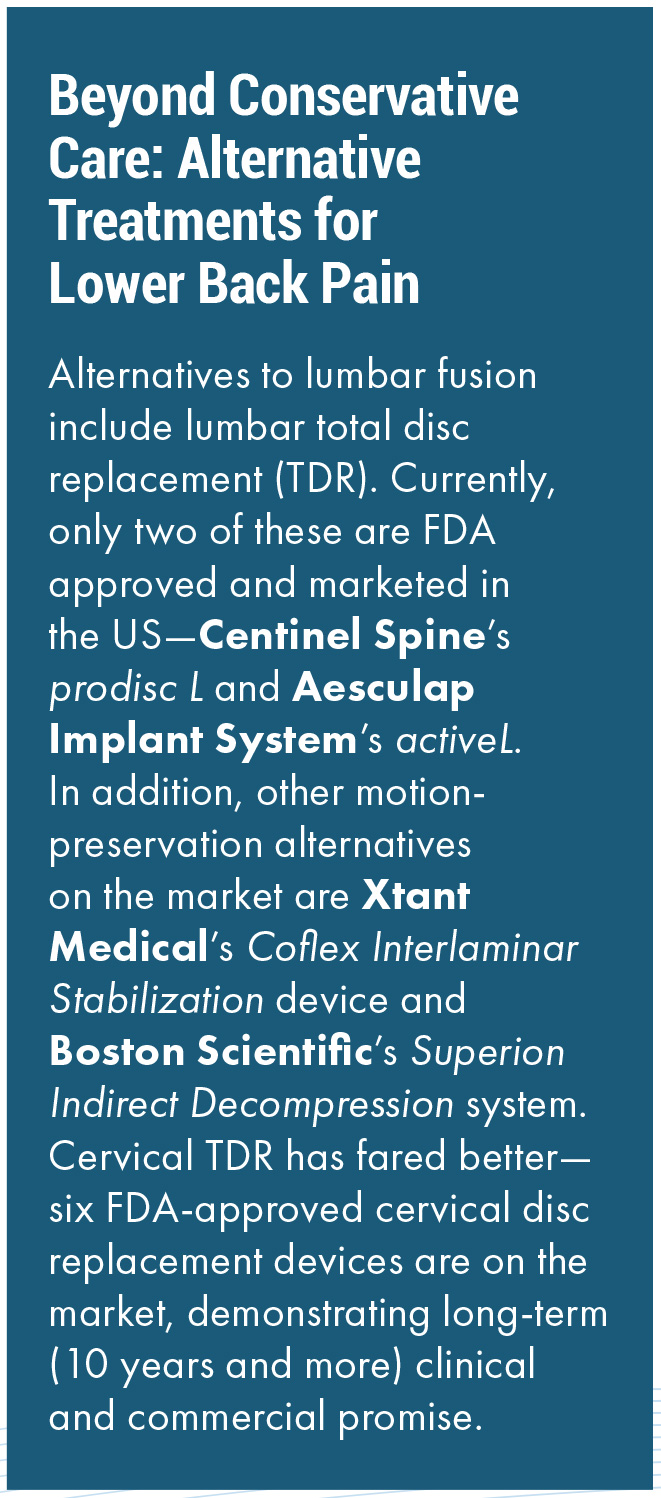

Intermediate alternatives like TOPS aim to overcome drawbacks of both procedures. Past efforts have had a tumultuous history, however, starting with the introduction in 2002 of the Charité lumbar total disc replacement (TDR), which aimed to  restore the normal function of a joint. Lumbar TDR’s adoption has been disappointing due to the complexity of the procedure and subsequent high complication rates (see Figure 1).

restore the normal function of a joint. Lumbar TDR’s adoption has been disappointing due to the complexity of the procedure and subsequent high complication rates (see Figure 1).

Other motion-preserving devices address earlier-stage moderate disease, avoiding fusion, but they cannot entirely restore joint function. These too have come up short as solutions and are limited in their use. The more severe patients eligible for these devices could be candidates for TOPS, Premia says.

The FDA approval for TOPS was backed by what experts say is a strong, well-designed clinical trial involving 321 subjects. An interim publication of the IDE results based on 249 patients (170 received TOPS and 79 were in the TLIF control group) demonstrated a statistically significant higher composite clinical success (CCS) score for TOPS patients compared with the control group (85% vs. 64%). All in all, TOPS patients got better faster, and had lower revision rates and less opioid use than the fusion control group, Sacher points out.

Moreover, the company was designated as a new technology add-on payment (NTAP) recipient by the Centers for Medicare and Medicaid Services (CMS), ensuring users get extra reimbursement for up to three years for their innovative inpatient procedures. NTAPs are meant to help hospitals cover the costs of targeted new technologies early in their lifecycle before CMS can update its base procedure reimbursement rates. The extra payments can play a significant role in early adoption of new devices.

Long-Term Commitment, High-Risk Bet

The TOPS approval is a personal and professional accomplishment for Sacher, who has pinned much of his career on its success. Throughout the two-decade process, he faced minefields that have entrapped other device entrepreneurs, but given his recent wins—the FDA approval, superiority claim, and NTAP designation—his strategy and attention to detail seem to be working.

The idea of a facet joint replacement for treating lumbar pathologies was first presented to Sacher at a North American Spine Society (NASS) meeting 20 years ago by Uri Arnin, a biomechanical engineer who was Impliant’s and is now Premia’s chief technology officer. At the time, Sacher, a Harvard MBA graduate, was the CEO of Impliant, the predecessor company to Premia. After meeting with key opinion leaders in spine surgery, Sacher and Arnin understood the need for a better treatment of diseased posterior elements of the lumbar spine for patients who were getting fused and were not doing well.

Sacher left Impliant in 2007 to co-found two other companies, which he and his partners sold to Boston Scientific and Spectranetics (now part of Philips). At the same time, Impliant progressed with its FDA clinical trial of the original facet replacement system but ran into financial troubles and shut down in 2010.

In 2011, Sacher committed his own funds to buy the assets of Impliant and started Premia Spine, buttressed by the interim US clinical trial data and positive feedback from participating surgeons on the original device. Under his leadership, Premia redesigned TOPS to make it smaller and simplified the surgical technique before relaunching it in Europe. Preliminary results from a European trial seemed promising, and the new product received the CE mark in 2012, but in the interim, the FDA recommended that a fresh clinical trial be initiated for the new TOPS system. Following renegotiations with the FDA, the TOPS prospective, randomized, multicenter clinical study began in 2017.

Sacher’s bet on facet joint replacement was and remains a high-risk proposition, to be sure. Despite its critical role in preserving spine motion, the facet joint has not been a focus of mainstream innovation, due perhaps to the complexity of spinal motion and the relationship of the facet joint to the rest of the spine. The spinal degenerative process begins when the disc height shrinks, which leads to changes in the position of the medial and lateral facet joints. This can result in abnormal articulation within the facet joints, affecting the cartilage and creating bone on bone articulation that leads to osteoarthritis and other painful conditions.

Moreover, even though the initial clinical data demonstrates that the TOPS device is safe and effective, the company still will have to convince surgeons, healthcare systems, which exert increasing control over surgeons’ selection of their equipment, and payors that the device is better long term than fusion and does not have the same drawbacks. Sacher, however, cites several precedents that helped to frame Premia’s strategies at key inflexion points, with design and evaluation of the pivotal trial being key.

The early 2000s were supposed to be a golden age of spine innovation, he says, but as efforts fell flat, investor appetite for the space dampened. While those setbacks created challenges for many entrepreneurs, which delayed fundraising and created a longer road to get to market, they also opened an opportunity for Sacher to buy a promising asset at a discounted price, and to make smarter decisions, based on positive and negative learnings from past experiences. (See "Cervical Spine Market: After Years of Effort, LDR Sees Payoff Ahead," MedTech Strategist, June 19, 2015 and "Positioning Paradigm Spine's Coflex for a Cost-Contained World," MedTech Strategist, January 17, 2017.)

Premia, and Sacher in particular, spoke with hundreds of patients and surgeons, especially as the company turned to direct-to-consumer tactics to entice reluctant subjects to enroll in its clinical trials. Patients had to be convinced that their participation in the trials was worthwhile, even though they stood a 33% chance of getting a traditional fusion versus TOPS, says Sacher, noting that “not one patient with whom I spoke to on the phone wanted to be in the control group—people do not want fusion—they want motion preservation.” The direct-to-consumer strategy was successful during the trial, accounting for over 25% of enrolled patients. The company plans to continue to respond to consumer requests for information on TOPS and direct them to surgeons who perform the procedure.

The TOPS clinical trial design and execution has been the biggest driver of company strategy to date. To manage the trial, Sacher hired the same team that had successfully steered the Coflex Interlaminar technology, an innovative motion-preserving stabilization lumbar device, through the process, enabling that device to gain FDA acceptance in 2012. That product, however, does not restore the full function of a joint.

For the TOPS trial, participating surgeons were evaluated to make sure they understood and were aligned with Premia’s technical approaches and clinical goals, including use of a “very wide decompression,” says Sacher—all but ensuring that the implantation, initially at least, would be an open surgery, inpatient procedure, even as the field of fusion in general is moving to minimally invasive surgeries in the outpatient setting. Surgeons also had to undergo training in a cadaver lab and agree to the use of a Medtronic or DePuy (Johnson & Johnson) pedicle screw and interbody system for the control arm—a stipulation some surgeons could not adhere to, given ongoing vendor contract consolidation.

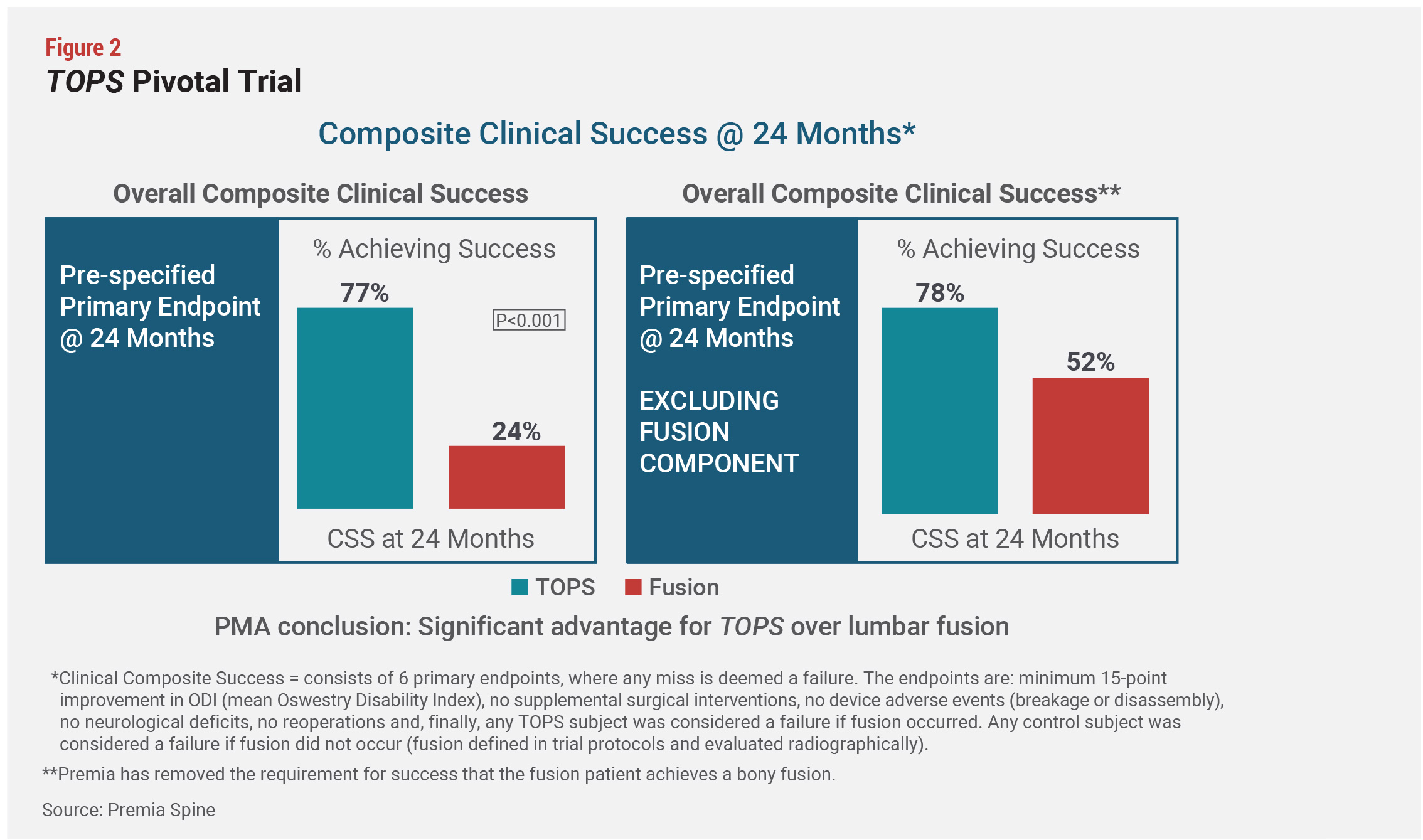

The pivotal trial for TOPS consists of 306 (321 ultimately enrolled) patients treated at 37 sites (50 surgeons) between 2017 and 2022. Patients were randomized to receive a TOPS procedure or the TLIF control based on a 2:1 ratio. Premia and the FDA agreed to use a composite clinical success (CCS) score consisting of six criteria, designed to reflect experiences among three key stakeholders: patients, surgeons, and radiologists—metrics that Sacher emphasizes are more stringent than what most companies rely on, which is typically a CCS comprising three or four metrics. The patient population was also more severely ill (as measured by Oswestry Disability Index [ODI] scores) than that in clinical trials supporting other spine devices, he adds.

The TOPS CCS included: an improvement of 15 points or greater in the ODI, a well-validated patient assessment questionnaire, neurological assessment by the surgeons, reoperation rates, device failure (breakage, disassembly, loosening, and lucency as evaluated by the radiologists), supplemental interventions, such as injections and nerve blocks, the presence of fusion in TOPS patients, and nonfusion in TLIF patients, and adverse safety events. Procedures were also assessed based on 11 secondary endpoints, including range of motion and pain. If any of the criteria missed its success threshold, the case was considered a failure (see Figure 2).

Based on compelling interim results, which showed a large divergence in outcomes between the two study arms favorable to TOPS, Premia, late in 2022, submitted expanded data to the FDA and switched its proposed labeling from noninferiority to superiority, says Sacher. This resulted in a regulatory approval delay but was worthwhile because “the company is playing the long game,” he states, and with that in mind, “it is better to launch with the superiority claim than to seek it later on, as we originally planned to do.”

Based on compelling interim results, which showed a large divergence in outcomes between the two study arms favorable to TOPS, Premia, late in 2022, submitted expanded data to the FDA and switched its proposed labeling from noninferiority to superiority, says Sacher. This resulted in a regulatory approval delay but was worthwhile because “the company is playing the long game,” he states, and with that in mind, “it is better to launch with the superiority claim than to seek it later on, as we originally planned to do.”

The clinical trial deliberately set a high bar for TOPS’ success, Sacher says--potentially a key advantage in a field that has traditionally been short on quality data. Although the FDA has well-defined criteria for device approvals, companies have some leeway to determine which metrics and cutoff points to use for assessing success.

The FDA ultimately based its PMA approval on a subset of 168 patients (115 TOPS, 53 fusion patients) for whom two-year follow-up data was available at the time of submission in 2022. Final results for all subjects will be reported likely in 2027, after the last enrollees in the trial have been evaluated for their mandatory five-year follow-up. In the product label, the FDA said that the “TOPS group demonstrated a clinically meaningful and substantial advantage over the Fusion control group, with 75.9% of subjects randomized to the TOPS group achieving CCS, compared to 23.9% of subjects randomized to the Fusion control. Based on these results the TOPS system was concluded to be superior to the Fusion control with respect to composite clinical success” while maintaining equivalent safety.

That said, Lahey neurosurgeon Ghogawala notes that although the FDA’s approval is a “big step forward,” the device still needs more studies to show that facet arthroplasty stabilizes the spine enough to significantly reduce reoperation rates compared with fusion or decompression alone. Some innovative devices like cervical TDR started to gain broad acceptance and to be on their way to becoming standard of care in spine surgery only after 10 years of follow-up data was published, but facet joint replacement likely does not need that degree of tracking to obtain mainstream adoption, Ghogawala says, in part because safety data exists from the device’s use in Europe. Still, he is waiting for five-year data on patients treated with TOPS before offering it in his practice. If they have substantially fewer reoperations than patients treated with decompression alone or with fusion, “this technology becomes very exciting as an option for patients,” he adds.

Ghogawala also questioned why lumbar fusion rates among the control group in the TOPS trial were much lower than the commonly accepted norms for this kind of surgery—making for a comparator that puts the TOPS device in a more favorably light. That fusion failure rate was "surprising" and needs careful evaluation to understand, he adds.

Premia CEO Sacher pushed back against this point, noting that even excluding nonfusion rates in the control group as part of the CCS, TOPS performed far better than lumbar fusion (78% success vs. 52% success in the control arm). And he understands that while some surgeons will be early adopters who are comfortable with using the device based on two-year data, others may want to see longer-term follow-up clinical trial results.

Whom to Target?

Gaining FDA acceptance is a critical milestone toward success, but far from a guarantee. Adoption by surgeons has proven to be as big a hurdle in spine innovation as regulatory achievements.

In determining its commercial strategy, Premia has a handful of examples to fall back on. Some of the most obvious are in the field of cervical TDR, and one that comes perhaps closest to Premia’s experience is Simplify Medical, which NuVasive bought for $150 million plus milestones in 2021 following the successful FDA approval and launch of the former’s CDR. (See “The Risk-Reward Ratio of Simplify Medical’s Comeback in Cervical TDR,” MedTech Strategist, June 13, 2019.) CDR had a long, steep climb to success, but is now poised to become standard of care for cervical spine patients, based on positive 10-year clinical trial data published beginning in 2019.

Indeed, many surgeons who adopt CDR are good candidates to target for TOPS because they “are building their practices around motion preservation and believe in it, but they do not have a good solution for lumbar fusion alternatives that preserves motion. The fact that they’re successful with CDR means that they have already probably fought the good fight with insurers,” says Sacher. Even so, his expectation is that building the market will take time, even with great clinical data.

Premia will use distributors to target surgeons and clinical sites that have become familiar with the technology through the ongoing clinical trials—including all the 37 clinical trial sites—plus another 18 surgeons who are trained on the procedure.

One bright spot for Premia’s device that neither Simplify nor Coflex has going for it is the presence of an NTAP reimbursement from CMS, worth up to $11,350, Premia says, to the facility beyond the DRG payment, which is an incentive for healthcare systems to try out the device. Reimbursement has often been a stumbling block toward achieving commercial success, with products like Simplify and Coflex struggling due to low CMS reimbursement. Lumbar facet replacement, in contrast, is “currently a green field that Premia has opportunity to dominate,” Sacher continues.

“The NTAP is a game changer that was not available to cervical CDR, which meant that doctors and facilities lacked incentives to make the transition,” he says. The NTAP starts in October and will last three years, giving the company time to negotiate a more permanent reimbursement with the potential for premium pricing.

In addition, according to Sacher, Premia lacks near-term competition. “We are 10 years ahead of competitors in this space, which gives us a monopoly that enables us to build a market and set the standard.” In comparison with CDR, he says, there’s less competition, better reimbursement, and bigger opportunity. “If we look at the pure number of patients available for CDR versus facet replacement, our market is 50% larger. We have an opportunity to be tremendously successful and drive this market space for at least a decade.”