ARTICLE SUMMARY:

Wall Street has not reacted positively to the news of the proposed Globus-NuVasive merger. Both companies must convince reluctant shareholders of the value proposition, given the history of disappointing deals in spine. Excerpted from our recent feature article.

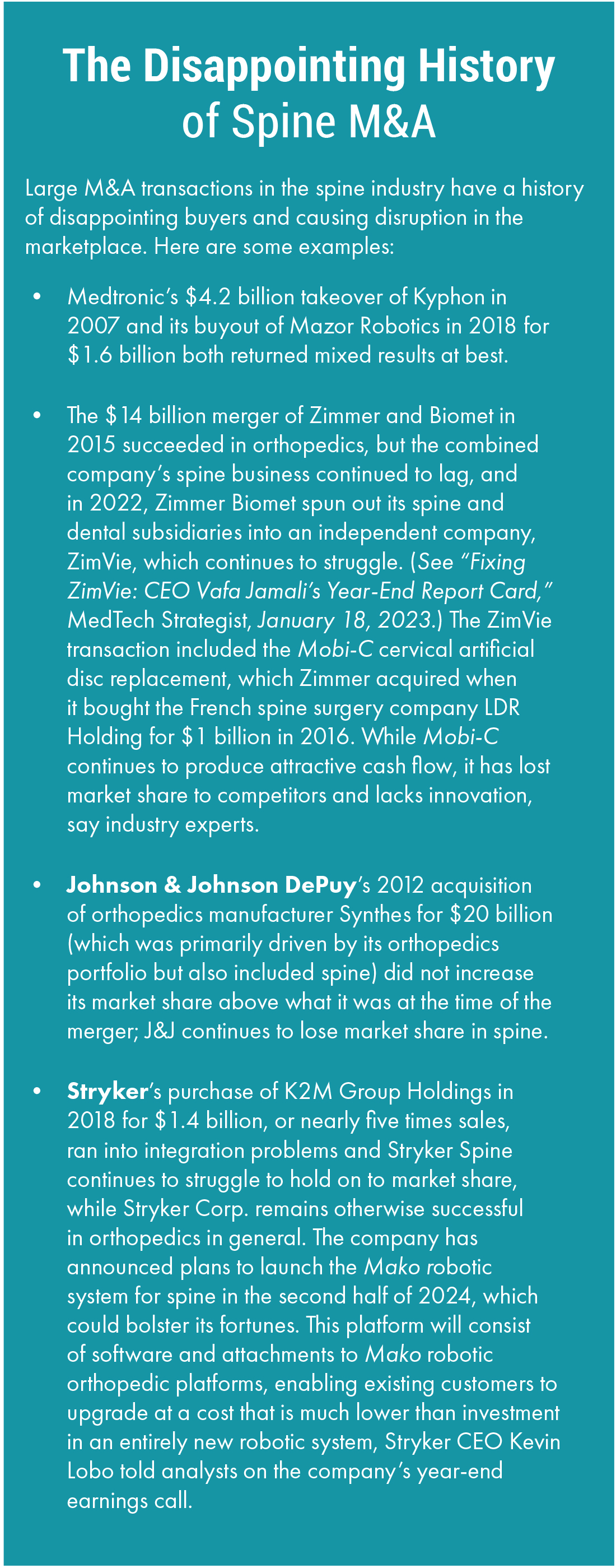

Spine mergers are inevitable, given the industry’s maturity, fragmentation, and lack of innovation.Globus Medical’s proposed buyout of NuVasive, announced in February, is the latest in a long list, and analysts have their own long list ofdisappointing deals in this space (see box). Reasons for these problems are multi-varied. The industry is fragmented, mature, and complex, characterized by the intricate nature of spine diseases, unmet medical gaps, and the continuing power of surgeon preferences and brand loyalties in buying decisions, even as large healthcare systems struggle to overcome financial pressures.

Spine conditions, in comparison with other orthopedic subsegments, have hundreds of diagnoses and nuanced approaches to treatment, resulting in demand for wide-ranging instrumentation variety. Surgeon-sales rep relationships are more consultative than other surgeries, even though technologies are mature, and innovation is stagnating. The deals almost inevitably require cost-cutting, which disrupts all-important sales channels and surgeon relationships. This creates opportunities for competitors to step in and woo talent, and that talent’s network of surgeons.

Spine conditions, in comparison with other orthopedic subsegments, have hundreds of diagnoses and nuanced approaches to treatment, resulting in demand for wide-ranging instrumentation variety. Surgeon-sales rep relationships are more consultative than other surgeries, even though technologies are mature, and innovation is stagnating. The deals almost inevitably require cost-cutting, which disrupts all-important sales channels and surgeon relationships. This creates opportunities for competitors to step in and woo talent, and that talent’s network of surgeons.

Globus and NuVasive combined would hold a roughly 20% market share. Estimates vary widely as to how much volume and revenues would be likely lost in the initial phases of the integration, with analysts putting the numbers at anywhere from 5% to 40% to 50%. The companies cite mid-2023 as the timeline for closing the deal but, for reasons mentioned earlier, many industry veterans are bracing for several years of inevitably heightened industry infighting.

A key question is how Globus will reconcile the 1,000-basis-point gap between its profit margins and NuVasive’s without disrupting the sales force and ultimately top-line revenue growth, analysts say. Although there are redundancies in the product lines, the companies say their strengths are complementary, not overlapping, so product line rationalization will contribute only a small amount to savings.

The market doesn’t place a lot of value on the rationalization of specific instruments, so bigger savings are more likely to come from realigning geographically overlapping sales channels, with some industry veterans arguing that Globus and NuVasive may be underplaying those concerns.

The integration of those territories also involves account managers and higher-level corporate executives, not just field reps, who have direct relationships with surgeons, points out one top strategic executive. He notes, for example, that rumors of mere interest in NuVasive caused Smith & Nephew’s stock to fall in 2019. This occurred even though the UK company wasn’t in the spine business, indicating just how disruptive Wall Street considers spine M&A.

Moreover, Globus uses a primarily direct sales model in the US, while NuVasive uses a hybrid model with a mix of direct reps and distributors—a strategy that is likely to change, if Globus’ previous preferences are an indication. The company laboriously converted its US distributorships to a direct sales model a few years ago.

“Management is fixed costs, and you do not go from 14% operating margins to 30% operating margins without making tough calls, says the industry executive.

“I guarantee you that Medtronic immediately started financial modeling the opportunity when this was announced,” says Chris Lyons, CEO of Southern Metrics Consulting, who previously worked as a top business development executive at Medtronic Spine & Biologics, adding that spine executives are expecting that “there’s going to be blood in the water.”

Trial MyStrategist.com and unlock 7-days of exclusive subscriber-only access to the medical device industry's most trusted strategic publications: MedTech Strategist & Market Pathways. For more information on our demographics and current readership click here.

Trial MyStrategist.com and unlock 7-days of exclusive subscriber-only access to the medical device industry's most trusted strategic publications: MedTech Strategist & Market Pathways. For more information on our demographics and current readership click here.