ARTICLE SUMMARY:

Medicare’s phased-in elimination of the inpatient only rule and simultaneous expansion of the list of procedures it covers in ambulatory surgery centers are forcing medical device manufacturers to rethink where and how much they get paid.

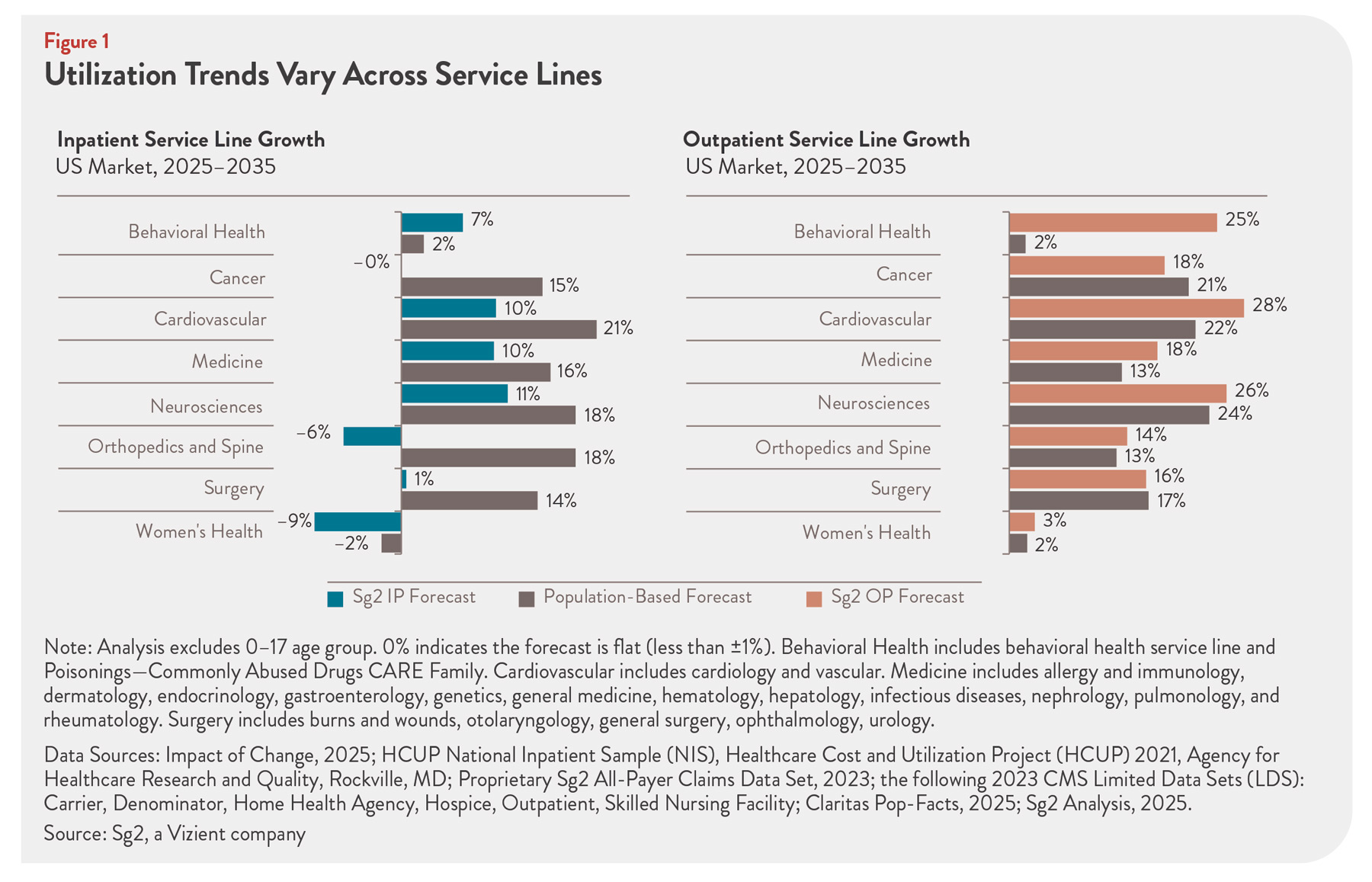

CMS’ stated goal is to move away from rigid requirements over the next three years toward greater reliance on physician judgment in choosing the most appropriate site of service, arguing that technology and practice patterns have outpaced 25-year-old safety assumptions (see Figure 1).

These gestures, combined with legislative proposals to implement site-neutral payments, which peg rates for the same service more closely across settings, are leading to long-term structural changes in healthcare reimbursement that have strategic implications for manufacturers. While the trends they tap into have been ongoing for years, they are accelerating and becoming more entrenched.

The first wave, effective January 1, 2026, removes all 285 musculoskeletal (MSK) procedure codes from the inpatient-only (IPO) list. With rare speed, the agency almost simultaneously assigned the majority of these codes—271 so far--to the Ambulatory Payment Classification (APC) buckets, which it uses to govern how ambulatory surgical center (ASC) procedures get reimbursed.

The first wave, effective January 1, 2026, removes all 285 musculoskeletal (MSK) procedure codes from the inpatient-only (IPO) list. With rare speed, the agency almost simultaneously assigned the majority of these codes—271 so far--to the Ambulatory Payment Classification (APC) buckets, which it uses to govern how ambulatory surgical center (ASC) procedures get reimbursed.

It also assigned several hundred procedures that are allowed in hospital outpatient department (HOPD) settings to the APC list for the first time, making them eligible for ASCs, including select cardiac surgeries. (See “Cardiac Ablation in More Places: Medicare Expands EP Access to Surgical Centers,” Market Pathways, February 16, 2026.)

At the same time, site-neutral payment policies are emerging as a potent disrupter of the current hospital-oriented system and portend a deeper economic fight rather than a technical coding tweak. Site-neutral payments are intended to pay similarly for the same service, regardless of setting (inpatient, hospital outpatient, ASC, or physician’s office).

Although these policies have yet to take effect broadly and remain controversial, early indications are that the payment rates will be at the low end of what industry hopes for.

For medtech manufacturers, these shifts are not abstract policy debates. Surgeons’ decisions on what equipment they use and where they operate—that is, in a hospital or HOPD setting, versus an ASC or physician’s office—are crucial to vendor economics. They affect long-term corporate strategy and day-to-day operations, surfacing repeatedly in legal and strategic conversations around the details of physician compensation, site-of-service strategy, and even as early as clinical trial design.

Companies are already thinking about where to run early clinical trials—inpatient versus outpatient—because these choices can shape downstream coding, coverage, and commercial positioning. While room exists for tactical course correction if safety or outcomes data from early IPO removals disappoints, the broader direction is clear: companies are aggressively exploring ASC-focused strategies and closer alignment with ASC surgeon-owners.

Some decision levers to watch include how codes are assigned to particular ambulatory payment classification buckets, which are groupings of similar outpatient services that play a role in determining facility fee rates; shifts in facility fee rates, which put downward pressure on ASC margins; and ASC ownership structures, which influence where surgeons perform their procedures and purchasing practices. Notably, physicians who own stakes in device companies often find it easier to use those products in their own ASCs than in large health systems, which may restrict physician-owned technologies over self-referral concerns—an under-appreciated driver of ASC adoption.

MedTech Strategist spoke to several experts on how these trends affect medical device manufacturers and the growth of ASCs. While medical device companies may be aware of these trends, a more nuanced understanding of them may help guide commercial strategy and procurement of medical devices.